1. Overview of Dubai property market 2026

Dubai’s real estate market in 2026 is not moving in a single direction—it is splitting into performance tiers. Some communities are experiencing strong capital appreciation and high transaction velocity, while others are stabilising or showing early signs of oversupply pressure. Data from Q1 2026 shows that the market recorded tens of thousands of transactions with continued growth in overall value, even as volatility increased in certain segments .

What stands out most is that demand is no longer evenly distributed. Instead, investors are concentrating capital in well-connected, lifestyle-driven, and yield-friendly communities such as JVC, Business Bay, and Dubai Marina, while peripheral developments are struggling to maintain pricing momentum. This divergence is shaping a “two-speed” property cycle across the emirate.

Transaction momentum

Transaction activity remains historically high, with off-plan dominating market volume. Developer-driven sales account for the majority of new deals, reflecting flexible payment structures and strong investor appetite for future supply . Communities like JVC and Business Bay consistently rank among the highest in transaction volumes, reinforcing their liquidity advantage.

Price performance snapshot

Price growth across Dubai in 2026 is moderating compared to earlier boom years, with most communities seeing annual appreciation in the 5%–15% range depending on location and asset type . Prime areas continue to outperform, while mid-market zones show more balanced growth.

2. Defining leading vs lagging communities

Not all Dubai communities respond equally to macroeconomic demand. The difference between “leading” and “lagging” areas comes down to structural fundamentals rather than short-term sentiment.

Leading communities typically combine high liquidity, strong rental yields, infrastructure connectivity, and sustained end-user demand. Lagging communities often suffer from oversupply, weaker transport integration, or delayed infrastructure delivery.

Key performance metrics

The market evaluates performance through a few critical indicators:

- Capital appreciation (price growth per square foot)

- Rental yield stability

- Transaction volume and liquidity

- End-user vs speculative demand ratio

- Infrastructure maturity

Communities that score high across all five metrics naturally attract recurring capital inflows, reinforcing their upward trajectory.

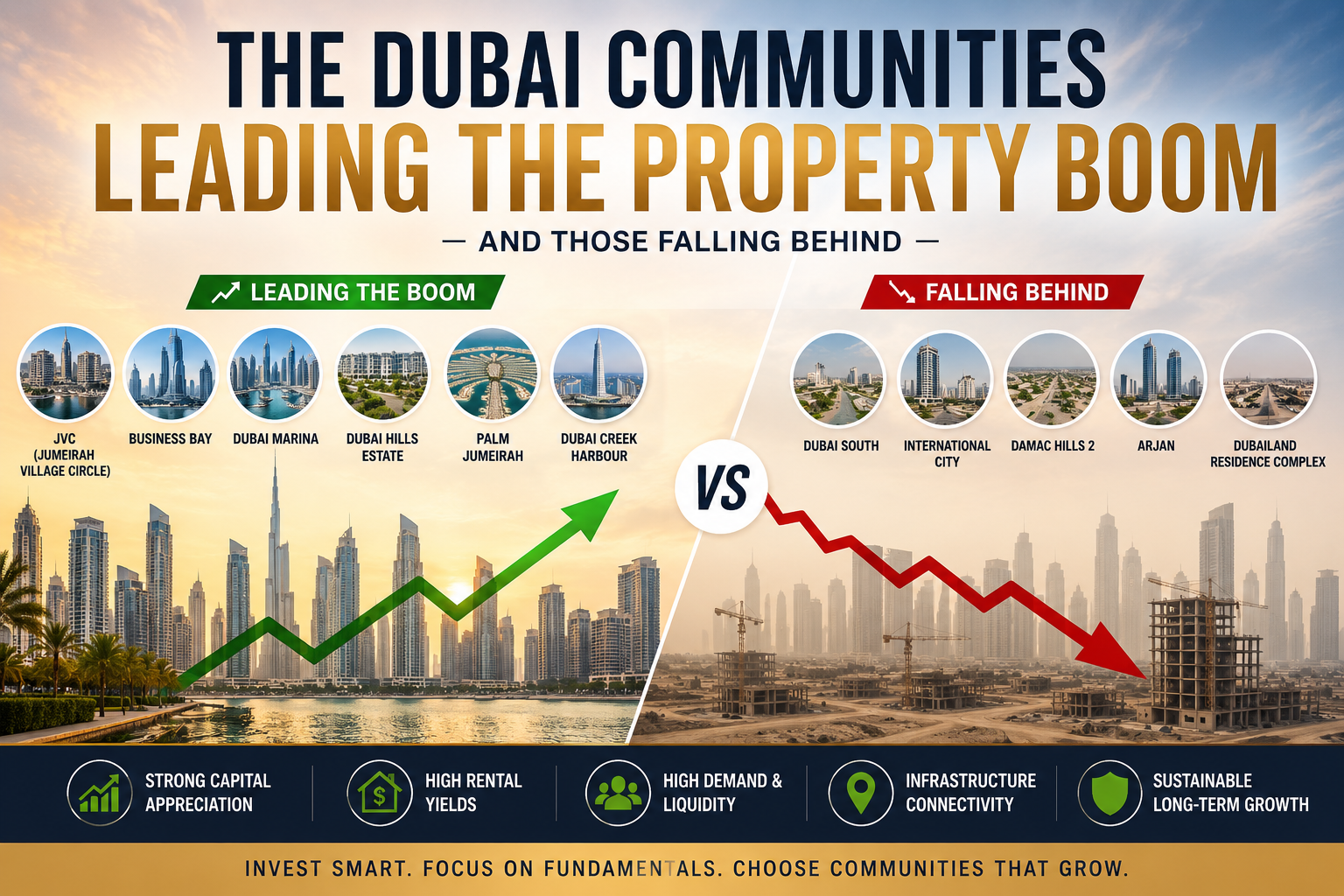

3. The communities leading the boom

Dubai’s top-performing communities in 2026 are not necessarily the most luxurious—they are the most functional, accessible, and investor-friendly.

JVC Jumeirah Village Circle

Jumeirah Village Circle (JVC) remains the undisputed volume leader in Dubai’s property market. It consistently records the highest number of transactions across the emirate, driven by affordable entry points and strong rental yields. Reports indicate yields often range between 7% and 8% depending on unit type, making it one of the strongest income-generating zones in the city.

What makes JVC dominant is its demographic balance. It attracts both first-time investors and long-term tenants, creating a self-sustaining ecosystem. However, rapid development also introduces selective oversupply risk in certain clusters, which investors must monitor carefully.

Business Bay Business Bay

Business Bay has evolved into a hybrid commercial-residential powerhouse. Its proximity to Downtown Dubai and DIFC gives it structural demand from professionals and corporate tenants. Canal-facing properties command significant premiums, reinforcing segmentation within the community.

Rental yields typically sit in the mid-to-high range for Dubai standards, while capital appreciation has remained steady due to continued infrastructure expansion and office demand. It is one of the most resilient “core urban” districts in the city.

Dubai Marina Dubai Marina

Dubai Marina remains one of the most internationally recognised waterfront communities in the region. It benefits from metro connectivity, high tourist inflows, and strong expatriate rental demand.

While price growth has slowed compared to earlier cycles, Marina remains a liquidity hub where assets can be resold quickly. This makes it a preferred exit-friendly market for investors prioritising flexibility over maximum yield.

Dubai Hills Estate Dubai Hills Estate

Dubai Hills Estate continues to dominate the family-end-user segment. Its appeal lies in its master-planned layout, schools, golf course, and integrated retail infrastructure. Demand consistently outpaces supply in villa and townhouse segments.

Unlike high-density communities, Dubai Hills offers long-term capital stability rather than speculative spikes. It is a “slow and steady” outperformer in the premium suburban category.

Palm Jumeirah Palm Jumeirah

Palm Jumeirah represents Dubai’s ultra-luxury benchmark. It attracts global high-net-worth individuals seeking waterfront exclusivity and branded residences. Prices per square foot remain among the highest in the region, supported by limited supply.

Although rental yields are lower compared to mid-market communities, capital preservation and prestige value make it a defensive luxury asset class.

Dubai Creek Harbour Dubai Creek Harbour

Dubai Creek Harbour is positioned as a future growth corridor. As development continues, early-stage investors are banking on long-term appreciation linked to waterfront infrastructure and skyline development.

It is still transitioning from a developing district to a mature residential hub, which creates both upside potential and short-term volatility.

4. Mid-tier stable zones

Mid-tier communities form the backbone of Dubai’s real estate ecosystem. These areas do not always dominate headlines, but they provide consistency, liquidity, and predictable rental returns.

JLT & others Jumeirah Lakes Towers

Jumeirah Lakes Towers (JLT), along with areas like Al Barsha and parts of Dubai Silicon Oasis, represent stable mid-market zones. They offer a balance between affordability and urban convenience.

JLT in particular benefits from lake views, metro access, and proximity to Dubai Marina, making it a consistent performer in rental demand. While capital appreciation is moderate, occupancy rates remain strong, ensuring steady income for landlords.

5. Communities falling behind

Not all developments are keeping pace with Dubai’s rapid expansion. Certain communities are experiencing relative underperformance due to supply pressure and slower absorption rates.

Oversupply zones

Peripheral master developments such as Dubai South, Dubailand, and select emerging corridors are facing increased competition from new launches. While infrastructure projects and airport expansion plans provide long-term catalysts, short-term absorption is uneven.

Some of these areas have seen pricing stabilisation rather than continued growth. In cases where supply is released faster than population inflow, rental competition intensifies, which can compress yields.

Investor sentiment in these zones tends to shift toward long-term capital growth rather than immediate returns. This makes them more suitable for patient investors with multi-year horizons.

6. What drives divergence

The gap between leading and lagging communities is not random—it is structural. Several macro and micro factors determine why certain areas outperform others.

Infrastructure & demand

Transport connectivity, especially metro access and highway integration, plays a major role in determining demand concentration. Communities near Sheikh Zayed Road corridors or metro-linked districts consistently outperform isolated developments.

Lifestyle infrastructure—schools, retail centres, healthcare, and leisure spaces—also strengthens long-term residency appeal. Meanwhile, investor sentiment is increasingly influenced by supply absorption rates and developer credibility.

Another critical factor is population inflow from expatriates and high-net-worth individuals, which continues to drive demand for centrally located, lifestyle-oriented communities. At the same time, speculative off-plan saturation in outer zones introduces cyclical pressure.

7. Investor outlook 2026–2027

The next phase of Dubai’s property market is expected to be less about rapid appreciation and more about selective growth. Investors are becoming increasingly data-driven, prioritising yield stability and exit liquidity over pure speculation.

Leading communities like JVC, Business Bay, Dubai Marina, and Dubai Hills Estate are likely to maintain dominance due to their structural advantages. However, returns will vary depending on entry price discipline and unit selection.

Luxury segments such as Palm Jumeirah will continue to attract global capital, but appreciation will be slower and more cyclical. Meanwhile, mid-tier and peripheral developments will depend heavily on infrastructure completion timelines and population growth absorption rates.

The key takeaway is that Dubai’s property market is maturing. It is no longer a uniform boom cycle but a segmented investment landscape where precision matters more than timing.

Conclusion

Dubai’s real estate market in 2026 is defined by divergence. Some communities are scaling new highs in transaction volume and rental demand, while others are stabilising under supply pressure. The winners are not random—they are consistently well-connected, high-liquidity, and lifestyle-integrated districts.

For investors, the message is clear: success in Dubai real estate now depends on choosing the right micro-market rather than simply entering the macro-market.

FAQs

1. Which is the best performing community in Dubai in 2026?

JVC and Business Bay are among the strongest performers due to high transaction volumes, rental yields, and accessibility.

2. Is Dubai Marina still a good investment?

Yes, it remains a high-liquidity market with strong rental demand, although price growth has slowed compared to earlier years.

3. Which areas in Dubai are underperforming?

Peripheral zones like Dubai South and parts of Dubailand are showing slower absorption due to rising supply levels.

4. What is driving Dubai property prices in 2026?

Key drivers include population growth, foreign investment inflows, infrastructure expansion, and off-plan developer activity.

5. Is Dubai real estate still profitable?

Yes, but profitability now depends heavily on selecting the right community and focusing on yield-positive assets rather than speculative flips.